Budget 2023 – Digital Public Infrastructure (DPI) the ‘Mantra’ for New India

iSPIRT Foundation, a technology think-and-do tank, believes that India’s hard problems can be solved only by leveraging public technology for private innovation. iSPIRT as a think tank pioneered the Digital Public infrastructure (DPIs)

India is at the cusp of what could be the most exciting quarter century of its post-independence existence, referred to as ‘Amrit Kaal’ by the Economic Survey yesterday and today in the Budget speech. The Economic Survey also mentioned that GDP could be boosted by 1% by Digital Public Infrastructure (DPIs), where India is stealing a March on the world for sure.

The second testimony to the important contribution of DPIs to the economy comes in the budget speech today when the finance minister stated, “India’s rising global profile is because of several accomplishments: unique world class digital public infrastructure, e.g., Aadhaar, Co-Win and UPI” in the forefront.

Development of DPIs, Stay-in-India Checklist (for Ease of Doing business of Startups), and a ‘jugalbandi’ between public technology and private innovation, through techno-legal regulations, are central to iSPIRT’s work in an attempt to build Product Nation.

The union budget 2023, brings in cheer to see attempts on the following:

Digital Public Infrastructure: The resolve to deepen the DPI and the belief in their role in economic growth. India Stack to build the DPIs has become central to the thought process. Taking the queue ahead the budget 2023 announced the development of DPI for Agriculture, which will be an open source, OpenAPI digital public good, to build inclusive farmer-centric solutions, credit & insurance, farm inputs market intelligence. An Agriculture Accelerator Fund has been announced to promote Agritech start-ups.

Vigyan Infrastructure: efforts to boost R&D, though limited to some sectors right now. Notable among these are – It encourages private sector R&D teams for encouraging collaborative research and innovation in select ICMR labs in the PPP model

One hundred labs for developing applications using 5G services will be set up in engineering institutions.

Center of Excellence for AI for “Make AI in India and Make AI work for India

MSMEs funding& growth is part of the budget thought process, which may lead to the use of another DPI called Open Credit Enablement Networks (OCEN) for enabling MSME funding.

The importance of Ease of doing business is reflected in some announcements like using PAN as a Common digital identifier and entity DigiLocker for MSMEs.

Wanting to keep the startup revolution going is reflected in the intent to use Startups to build technology in multiple sectors and also use the policy for a new India.

However, beneath all the euphoria, some chronic issues remained to be addressed. The disappointment is on the Stay-in-India checklist (a list of Ease of doing business issues for Startups) to stop startups from slipping from India, which has not been addressed. The checklist is being continuously pursued by iSPIRT and is much needed to provide a competitive edge for India to refrain startups from leaving her jurisdiction.

Overall it’s heartening to see the vision statement in budget, “Our vision for the Amrit Kaal includes technology-driven and knowledge-based economy”.

About iSPIRT Foundation – We are a non-profit think-and-do tank that builds public goods for Indian product startups to thrive and grow. iSPIRT aims to do for Indian startups what DARPA or Stanford did in Silicon Valley. iSPIRT builds four types of public goods – technology building blocks (aka India stack), startup-friendly policies, market access programs like M&A Connect and Playbooks that codify scarce tacit knowledge for product entrepreneurs of India.

India currently has90 unicorns – startup companies that are valued at over $1b – and will likely soon have 100 unicorns, becoming the third such country after the USA and China. Since January 2016 when the “Startup India” program was launched, the startup ecosystem of India including infrastructure for startups, be it incubators, mentorship, funding, corporate initiatives, media coverage, or even patent filing, has improved substantially making life easier for entrepreneurs.

However, it is still not as smooth a ride for the Indian start-ups as it is for startups in the advanced economies of say, the USA, Singapore, and China. Our “ease of doing business” is yet to be on par with the developed world, especially given the high taxation, onerous compliance requirements, inadequate and cumbersome legal protection of IP, as well as time-consuming and expensive processes to access capital and secure exits. It isn’t a surprise therefore that many companies are shifting their primary legal location to foreign jurisdictions like the USA, and Singapore.

How do the numbers stand?

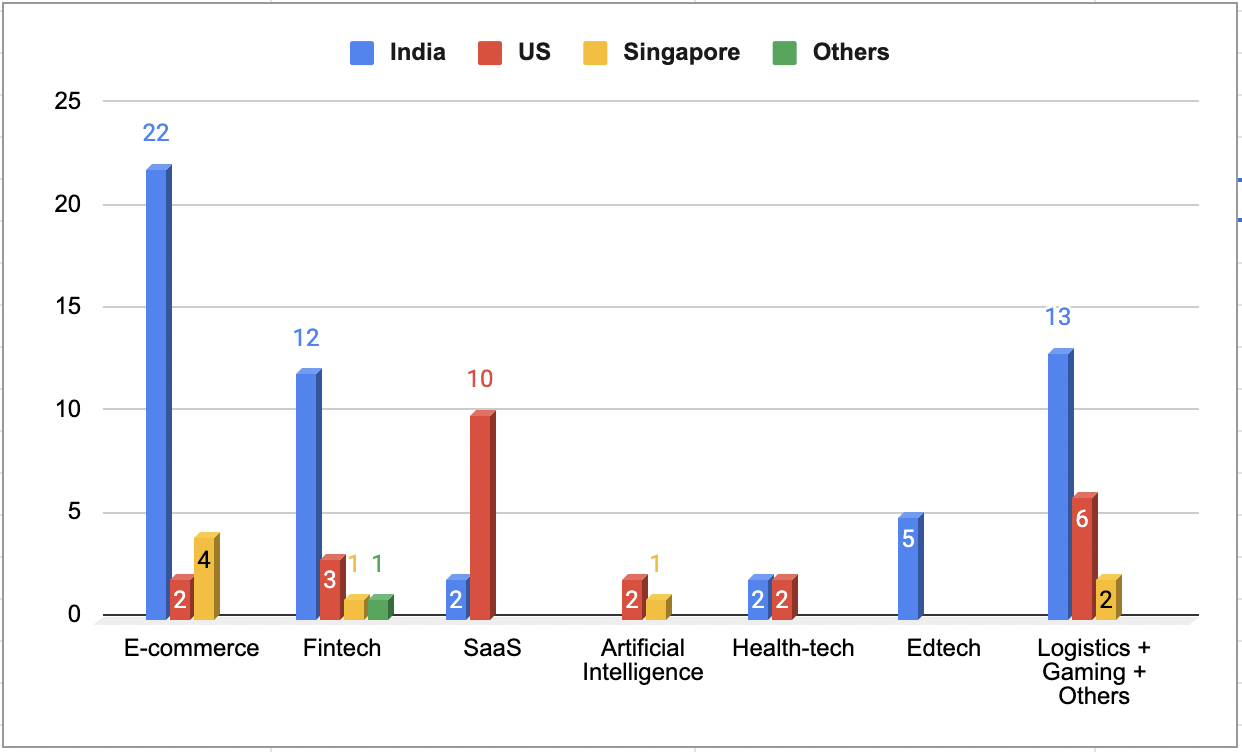

As per a study by Venture Intelligence, of the presently known 90 “Indian” unicorns), 56 are based in India, 25 in the USA, 8 in Singapore, and 1 in the Netherlands spanning sectors from e-Commerce to fintech to gaming and more. In other words, 38% of “Indian” unicorns are not quite Indian as they are domiciled outside of India. Moreover, these 34 unicorns have raised approximately $30B ie, this large money could have been but hasn’t been invested into an India domiciled entity.

Sector Wise break-up of the Unicorns

Source: Venture Intelligence

Chart: Sector-wise domicile of unicorns as on 31st March 2022.

The reasons for incorporating in the USA are different from incorporating in say, Singapore. SaaS founders find it easier to reach out to the large market for SaaS “Software as a Service” based offerings in the USA by incorporating there. Companies incorporated in Singapore for high “ease of doing business”, low taxation, quality infrastructure, and quality of life while remaining close to India.

Out of 12 Indian unicorns in the SaaS category, all except Zoho and Darwinbox are based in the USA. SaaS offerings are expected to be a $1 trillionopportunityand India will lose wealth creation, tax revenues, listing, and related income, by not having these companies domiciled in India.

Of the three unicorns in a frontier technology area like Artificial Intelligence, namely – Glance, Fractal, and Mindtickle, one is registered in Singapore while the other two are in the USA. Of the 3 unicorns in Gaming, Mobile Premier League and Dream 11 are based in Singapore and New Jersey respectively while Games 24×7 is registered in India.

Flipkart, India’s greatest startup success story and the poster boy for Indian e-commerce, which was acquired by Walmart at a valuation of over $20B, was domiciled in Singapore. That set the trend of e-commerce companies having their HQs in the island country. There are many Singapore shell companies set up by VC funds to become holding companies for Indian subsidiaries. Singapore is today the hottest destination for the registration of Indian e-commerce players.

Even more worrying than this trend of registering the parent company outside India is the migration of startup founders to UAE and Singapore. Lower taxes, easier access to capital, government support, simple compliance, and better quality of life while being just a short flight away from India make the UAE and Singapore rather attractive to founders.

Whichever country our startups chose to register or our founders chose to migrate to, the ultimate loser is India with intellectual property ownership and funds being vested in non-Indian jurisdictions.

Stay in India Mission

In order to retain the economic value added by the start-up ecosystem, it is important that India urgently puts in place policies that ensure that founders and startups ‘Stay-in-India”. This will require the coming together of various ministries, particularly DPIIT/Min of Commerce, Ministry of Finance, Ministry of Electronics and Information Technology, and regulators like the Reserve Bank of India and Securities and Exchange Board of India to address the Stay-in-India Checklist.

Stay-in-India is an evolving checklist of issues that need to be solved to contain the exodus of startups from India. These issues fall under four categories: a) Ease of doing business and making it easy to raise funds; b) harmonization of coding of digital economy c) Reducing overall tax anomalies and d) Increased DTA and foreign markets access.

The issues are comprehensively listed in the Stay-in-India checklist.

As an example, let’s consider the anomalies in the taxation of dividends. Dividend received from overseas subsidiaries, that has been already taxed, is taxed once again in India as income in the hands of the company. Also, while the rate of tax on such dividends for certain companies is 15% (as against 30%), the same exemption is not provided to limited-liability partnerships and individuals. It amounts to double taxation of income and discourages a model where overseas subsidiaries of Indian startups can pay dividends at lower tax rates to Indian shareholders. Removal of this dividend tax will directly encourage start-ups to remain domiciled in India and receive dividend income from subsidiaries abroad.

Similarly, there are regulatory frictions e.g. TDS on the sale of software products which reduces the working capital in hands of Software product companies, or the need for filling the Softex form (which was relevant in the early days of IT services exports), and which is now redundant as GSTN Invoices already have the required and sufficient data. All that is required is for different departments of the Govt and regulators to connect digitally and share information. The unfavourable tax regime for IPR protection, such as subjection to minimum alternate tax, IPRs being subject to income tax, and not capital gains even when they are held for more than a year is another big irritant. Technology-heavy startups, therefore, tend to relocate to jurisdictions like Singapore and the USA that have a smoother and lower-cost approach. Founders relocating to overseas jurisdictions are typically seen around the time of M&A. One of the reasons relates to taxation: typically, a portion of the financial proceeds arising from an M&A transaction is held in escrow and released to the founders after some time and/or completion of certain contractual obligations. The escrow payments are treated as income by the Indian tax authorities rather than capital gains as other jurisdictions do – this needs resolution.

India is emerging as a global startup hub, with the support of the Govt, with our startups attracting capital and talent while being at the forefront of innovation, jobs, wealth, and intellectual property creation. Brand India is enhanced globally by the success of Indian startups. With more support from the Government by way of removal of regulatory friction and by providing incentives – fiscal and regulatory – the ecosystem required to create, enable and grow Indian startups will dramatically accelerate.

The Ease of Doing Business must be tackled in mission mode with the Stay-in-India Mission (SIIM) being an integral part of India is to secure its rightful place around the global innovation table.

Disclaimer: The article depends upon various pubic data sources apart from credible data sources that are relevant at the current date and time. Readers may like to read this accordingly.

The payment gateway problem in exporting online from India

It is not easy for Indian Software product companies to export products online and receive payments in India. This is true for both the downloadable Software product or Software as a Service (SaaS).

Experts say there is no legal or policy hurdle from RBI. Yet, there is friction. An Indian payment gateway service provider denies foreign currency cross-border transactions from India to a startups or small company. Only exceptions could be some large companies.

As part of ‘PolicyHacks’ at iSPIRT, we attempted to attend to the issue of recurring billing in a previous blog here. This blog is another continued effort in this direction. It is based on a discussion with experts from payment solution companies. Embedded below is a video discussion with Krish Subramanian, Cofounder of Chargebee and Kiran Jain of Razorpay.

The options available and adopted by most small Software product companies’ today are:

Use a foreign payment gateway like PayPal, 2 Checkout, Skrill etc. Or

Setup a branch office or a subsidiary in a foreign country

Incorporate in a foreign country and sell globally from there including India

The option #1 above of using international payment providers comes with a heavy transaction cost. The services are not of same order as one can avail being in US or Europe.

So, option #2 and #3 becomes much attractive. This leads to exodus of Indian Software product company’s to USA, Singapore or Europe etc. India stands to lose in the game.

Krish mentions that, “the Indian companies are forced to move abroad to seek the frictionless experience in the payment part, where they allow month on month and do seamless upgrades and downgrades”. He further adds up, “Indian companies being in India do not get the level playing field, even when the strengths of product are very similar to a foreign product. Even using a solution like 2Checkout being in India does not provide seamless upgrade and downgrade. Hence, many companies go and incorporate outside”.

This problem, therefore, is one of the ‘biggest hurdle’ to the ‘stay-in-India’ concept for startups. It is vital that policy makers pay attention and remove friction to this problem for startups to believe in ‘India Story’.

Kiran Jain of Razorpay mentioned that the added attraction for Indian Software product company to move abroad is that, “an Indian company selling on international payment gateway from outside India does not have to comply with service tax”.

This is another level playing field problem. Being in India the Software product sales online is subject to service tax. On other hand being a foreign incorporated company and selling a B2C product the service tax is totally exempted. This is so in current policy framework and is going to stay same in the proposed GST framework.

Although, this is not directly related to the payment gateway problem, it does add-up to the exodus of Startups problem. This issue has been covered in an earlier blog here. It is a policy agenda item on list of taxation issues (of iSPIRT) to be addressed by Government of India and also an item on Stay-in-India checklist.

The cross-border online trade of Software product is directly a Payment Gateway issue. Let us further understand what are the underlying causes, policy issues, possible resolutions and suggestions.

Is there a regulatory hurdle? If not, then what is the cause of problem?

Kiran says, “RBI came up with OPGSP guidelines in 2014”. And, “this policy allows the operation of International payment gateways”, that can facilitate both the foreign currency cross-border transactions and recurring billing. According to Kiran, many Indian banks have capability to provide platform which can accept international cards and multi-currency systems. Few banks support up to 17 different foreign currencies, though the settlement is all done in US dollars.

Why are banks not giving it? Kiran said that in last one year in USA, out of $28.33 trillion online transactions, $16.33 billion were classified as frauds. Indian banking system does not have a capability to incur such losses, “that is the threat to Indian banks”. This threat is the result of ‘returns’ or ‘charge-back’.

In case of delivery of downloadable Software product, at least there is a trail of transaction that can establish that the Software was really downloaded and if unsuccessful the Software can be delivered again. However, in case of services it may be difficult to handle the consumption trail at least in B2C transactions. In B2B transactions, such problems normally do not arise.

Hence, handling the risk of returns and charge-backs is the problem to solved. Solving this will encourage India banking systems to offer free and fair cross-border international payment gateway services.

What is the solution to problem?

Large players by virtue of volume or by offering a risk covering instruments can easily avail the service from banks themselves.

Small and Medium players can use payment aggregators. PayPal and 2Checkout are nothing but aggregators. Thy have infrastructure built in USA. In India they provide services under OPGSP guidelines. Their relationships with issuing banks in USA enables them to provide services in India.

Kiran says, “as on date we have many aggregators in India”. But, “we have not seen any Indian aggregator moving to US and partnering with banks like Wells Fargo or Worldpay”, who could build “an infrastructure trail in US and bring it to India and start providing cross-border payments”.

This will be a powerful option according to Kiran. This option can be used to ease out cross-border multi-currency payment system aggregation. This will give exporters alternative to PayPal and 2Checkout etc.. This will also reduce transaction costs by at least 30%. Now, an Indian merchant pays 4 to 6% plus the currency conversion costs as a compared to the 2.9% + 30 cents per transaction in USA.

The other advantage of Indian aggregator with US infrastructure will be the better understanding of the Indian merchants and the risks involved. Hence, better placed to manage the risks. “Today PayPal looks at every merchant as risky merchant”, says Kiran. The Indian players can have option of either aggregating the merchants on PayPal model. Or offer facility directly to mid and large players. In later case the entire risk engine is managed by the aggregator. The risk engine will take care of detecting the fraud cards, stolen cards, charge-backs cards as these will not be the capability of a merchant.

In the aggregator model, it is possible to play on volumes by on boarding a large number of small and mid-size merchants. This way an aggregator can easily go to a bank and say my charge-back to sales ratio is just about 1.76%.

Kiran further adds that as an alternative risk mitigation mechanism an Industry body could register small and mid-size Software product companies (merchants) and provide some kind of a certified credit rating. This could help banks and aggregators to assess the risk associated with the individual merchant.

Krish feels, a Govt. body like MSME could build a registration system of merchants with past history, people involved etc. (this could be like extending the Performance and Credit rating scheme of MSME). “This could act as a KYC”, says Krish for the aggregator, payment gateways and banks.

Are there Indian Aggregators offering such services?

As mentioned above, banks offer services in a limited way to large merchants. Aggregators like RazorPay also provide services but again with conditions attached.

Kiran says,“Razorpay provides the services on selective basis. We do not offer the option of card details to be held by merchants”. He further informed that merchant account with many charge-backs are suspended and that cases with one-off charge types may be allowed.

So, there is conditional availability of Indian service providers of cross-border online payment gateways.

Concluding remarks and iSPIRT views

“It is a crying shame if many startups still incorporate outside India just to get a level playing field”, says Krish Subramanian. He also listed following observations:

there is an option that is emerging (in terms of aggregators);

there are no regulatory hurdles per say;

it is more about risk mitigation;

the risk mitigation is about creating awareness by closely working with banks;

it is also about creating awareness amongst merchants themselves to be able to understand reasons why banks act in certain way and about clarity on pricing, return and refund policy etc.

creating overall awareness in eco-system

iSPIRT views on the overall situation on the given problem and present policy status are as follows:

For India to be a Software product nation, Indian resident companies should be able to carry out cross-border trade and receive foreign currency payments onlineseamlessly without opting for incorporating a subsidiary outside India

For a healthy Software product ecosystem, it is vital that Software product companies have access to several options of payment gateway service providers with differing service offerings

RBI alone cannot solve this problem.RBI policy of OPGSP allows the payment gateway players to provide services in India. The inherent risk does not encourage service providers to offer cross-border payment services. RBI may have to become more reformative in encouraging Indian international payment gateway providers.

Government of India needs to intervene and devise an integrative policy that:

promotes an ecosystem of Indian cross-border payment providers

build a mechanism that helps banks and OPGSPs to mitigate their risk without hurting consumer interest

support Software product companies in their cross-border trade by a proactive policy

MeitY can incorporate enabling policy measures in National Software product policy and offer an Indian Software product company registry that has an inbuilt mechanism to ascertain and certify a Software product company’s credibility. Also financial instrument like an Industry corpus fund could provide a common bank guarantee, that can be backup with surety bonds from individual product companies for a defined threshold.

In a digital world order, cross-border trade is going to be highly dependent on easy availability of international payment solutions. Indian merchants able to scale their international trade with ease is vital for India to be retain leadership in Software trade.

This write-up should be read along with the previous blog – The Value Added Service Providers in Cloud Telephony. These blogs help us to accumulate the progressive development in discourse on policy for this segment of Industry. It is important for our common understanding and help Software product industry innovating in telecom sector in general and cloud telephony in specific terms.

The Startups providing Value Added Services also refereed to as Cloud Telephony submitted their response to Consultation Papers by TRAI on Voice Mail/Audiotex/Unified Messaging Services Licence.

TRAI also received responses from other service providers (which includes licensed Telecom Operators and ISPs) and Industry Bodies and Individuals. iSPIRT response was also submitted on the due date and can be accessed here from TRAI website.

The responses have been analysed and as required the counter comments have been filed with TRAI. Given below is our Response submission.

Counter Comments to responses received on Consultation paper by TRAI on Voice Mail/Audiotex/Unified Messaging Services Licence. Dt. 08/08/2016

After reading the responses to consultation papers, it is evident enough, that there is a clear divide between the Startup or SME players and the Telcos or the industry bodies representing them.

As previously described by us, almost all companies presently providing the services in this (voice mail/Audiotex) space are startups or SME players who have built their own Software products. Unified license operators are already allowed to provide these service. So, there is no barrier for them to enter in to these services, except creating specialisation around these services and building the requisite Software that runs the service.

The licensed Telecom operators in their responses to consultation paper have blindly favoured a license regime in this space, as well as attempted to make the case of revenue loss and breach of license. This is clearly an attempt to hog the telecom sector landscape.

We believe the approach taken by the large players in the Industry is contrary to the direction, thought and objectives of present Government. It confronts the principles of building an innovative society and multiplying growth opportunities for the enterprising youth of our country.

Recognize them as value added Services

We already stated this in our response earlier submitted. However, it seems there is a need to reinforce the point.

The services provided in this space are highly specialised “Value Added Services”. They are by no means either the carriage services or network services. It is a layer on top of the existing mobile and basic telephony that delights the consumer by fulfilling their needs that basic/mobile telephony cannot.

Value Addition is done on the services hired from licenses telecom operators, which have already been subject to revenue share mechanism. Hence, the very claim that these services can be sold at a cheaper rate than the local calls is squarely an imagination. So, also the revenue loss story does not stand any ground.

Therefore, the need to recognize this aspect of “Value Added Service” providers, is primary to any policy framing under consideration on the subject.

Regulate doesn’t imply inevitability of license

There is a serious need to catch up with technological advancements. A large country like India can’t be left to mercy of few companies on this account. This calls for reform and further deregulation of the telecom sector to a degree that it is accommodates the changes from time to time.

In order to allay any doubts of the stakeholders in this sector and better value to the consumer, there may be need to regulate this sub-sector of Value Added Service provider.

Regulation does not always mean “a license”. This value added service sub-sector does not hurt the incumbent licensees in any way. Hence, a simplified regulated regime with lower administrative burden and lowers costs is desirable for suitability to this segment of the telecom sector.

Hence, a registration system with period monitoring and control rather than a license regime has been recommended by us.

Promote Innovation in Digital economy

Indian is entering in to a ‘Digital Economy’ era. Digital India is also not just about connectivity and switching networks. So, a ‘Digital India’ cannot be created by just handful of licensed Telecom players. The consumer in a digital economy is going to consume variety of data and application. Innovative Software products can power up the Digital India to make it a functional ‘Digital Economy’.

Innovation is going to be the lubricant of future digital economies

This segment of the Value Added Service has been born out of innovation of individual entrepreneurs and service provision works on Software products. So, also the commercial part of the service in integrated manner.

At this juncture, when India is wanting to unleash the innovative power by its StartupIndia policy, the license raj or barrier created by large Telcos can be counterproductive to digital economy or the Digital India dream.

Telecom sector and telecom policy at large has to imbibe this need to create friendly promotional environment for innovation to happen. It is not hidden from any one that innovation worldwide is being driven by individuals and small players.

All stakeholders in telecom sector including the licensed telecom operators should contribute to Innovation. Hence, the need to support these small Value Added Service providers and welcome the new ones to emerge.

iSPIRT Request

We seriously feel that growth cannot come from fixing ourselves to status quoist approach. There is a need to further add value to the telecom sector and hence a need to create scope for number of small players to contribute to the overall telecom sector.

There is a huge opportunity for Indian Software industry to innovate and contribute to telecom sector. We from iSPIRT, request that TRAI takes the above points and our earlier response submitted in to consideration and create an enabling environment for India to grow.

In this session on Domestic venture debt, we talk about a recent announcement by Government of India, that relaxed the provision on raising debt from domestic non-banking sources of funds. Sanjay Khan speaks on the subject in below embedded video.

What is the problem, that this new announcement on domestic venture debt solves?

Private companies can raise debt funds in a restricted manner only. They could raise debt from some allowed sources. These could be like company directors, their relatives and other companies etc. But, not from sources like angel funds, domestic VCs who are not companies. A debt raised from such sources fell under deposits category.

To accept ‘deposits’, companies need to follow number of conditions, which are quite tedious.

What is the new announcement?

As per sub-clause (iii) of Clause 68 of Section 2 of Companies Act, 2013 definition of Private Company, “means a Company which by its articles prohibits any invitation to the public to subscribe for any securities of the Company”.

The new announcements open up some new avenues of raising debt funds from domestic markets.

These new sources of funds, added to this non-public funds category are funds registered and operating under SEBI’s regulated regime. Following are these three new sources

1. Alternative Investment Funds (AIFs)

2. Domestic Venture Capital funds

3. Mutual Funds

Prior to this announcements funding from these sources was treated as deposits and not loan.

What are the limits of announcements?

Whereas this announcement opens up these three highly potential sources of domestic debt funding, it is limited to Rs. 25 Lakhs only.

So the announcement is likely to benefit startups in their early phase.

The other good part is that, this is not limited to recognised Startups or startups registered under StartupIndia with DIPP. It is open to any private company hence it can apply to any startup.

The announcement adds up to efforts made by Government of India in creating better environment for funding. It is a step forward in the direction.

iSPIRT believes and is further taking up with the Government to not limit this provision to Rs. 25 lakhs.

The video below covers this topic with Sanjay Khan, the expert who was instrumental in building up the stay-in-india checklist of iSPIRT.